“A forecasting model is a formalized description of the relationship between what we observe has happened in the past and what we then think may happen in the future.”

Jennifer L. Castle et al.

-

-

A free book on forecasting with Python is available online.

If you’d like to learn the foundations of forecasting, take a look at:

https://otexts.com/fpppy/ -

How is value distributed within a day, a week, a month, a season, or a year?

I like this question because it sharpens the analysis of spot prices. The total value across the entire period is normalized to 1 (or 100%), making it possible to examine how much of the total value is represented by individual hours or intervals.

Instead of looking only at absolute prices, the focus shifts to the share of value each period contributes to the whole.

-

“Transformations such as logarithms can help to stabilize the variance of a time series. Differencing can help stabilize the mean of a time series by removing changes in the level of a time series.”

Transformations such as logarithms help stabilize the variance of a time series by reducing heteroscedasticity, while differencing removes trends and level shifts to stabilize the mean. Applying both transformation and differencing yields a series with approximately constant mean and variance. -

grok:

“An Hourly Price Forward Curve (HPFC) is a high-resolution forward price curve specifically constructed for electricity markets, providing expected (or market-implied) electricity prices for each individual hour into the future — often from day-ahead out to several years ahead (commonly 3–5+ years).It serves as one of the most important building blocks in modern power trading, origination, asset valuation, PPA pricing, battery/storage optimization, and risk management in deregulated electricity markets.

Why electricity needs something more granular than a “normal” forward curve

In most commodity markets (oil, gas, metals, agricultural products), forward prices are quoted for relatively large delivery periods:

- Months, quarters, or calendar years

- A single price often applies to the whole period

Electricity is fundamentally different because:

- It cannot be stored economically at scale (at least not until very large battery deployment in the 2020s)

- Supply and demand must balance every second

- Prices show extremely strong hourly, daily, weekly and seasonal patterns

- Negative prices, price spikes to thousands of €/MWh, and huge intra-day volatility are common

Standard futures contracts in Europe (EEX, Nasdaq, ICE, etc.) are typically settled on base-load (all hours), peak-load (e.g., 8–20 h), off-peak, or sometimes block products — but almost never on true hourly granularity far into the future.

→ The market gives you block-average prices for future delivery periods, but real-world exposure (load, renewables, storage, demand response) is almost always hourly-shaped.

The HPFC solves this by disaggregating / reshaping the observable futures prices into a synthetic hourly price series that:

- Exactly reproduces the market prices of all traded futures / forward products when you take the appropriate hourly averages

- Embeds realistic hourly seasonality patterns (intra-day shape, weekend vs weekday, summer vs winter shapes, etc.)

- Is usually arbitrage-free with respect to the observable market

Core components typically used to build an HPFC

Most commercial and proprietary HPFC construction methodologies combine:

- Market prices of futures/forwards (the hard constraint — the curve must match these when averaged appropriately)

- Yearly, quarterly, monthly, weekly base / peak contracts

- Historical hourly spot price patterns (to extract typical intra-day, weekly, seasonal shapes)

- Fundamental drivers / forecasts (in more sophisticated models)

- Expected residual load

- Renewable generation profiles (solar, wind)

- Fuel & carbon prices

- Outage schedules, hydro availability, cross-border flows, etc.

- Mathematical reconciliation (optimization / calibration)

- Often least-squares fitting, Bayesian-like blending, quadratic programming, or machine-learning-based calibration

The result is a long time series (e.g., ~44,000–50,000 hours for 5 years) of hourly prices that:

Shows realistic hourly variation driven by historical / fundamental patterns

Matches all observable futures prices perfectly (or within very tight tolerance)”

-

I will review several chapters of Forecasting: Principles and Practice by Rob J. Hyndman and George Athanasopoulos.

-

“Commodity price risk is an important element of the world physionomy at this date”

“Every commodity is traded on a spot market.”

“A need for standardization in terms of quantity, quality, delivery date emerged and led to the establishment of the New York Cotton Exchange (NYCE) in 1842″

“Let us observe that the fact that any transaction on commodities may be physical (delivery of the commodity) or financial (a cash flow from one party to the other at maturity and no exchange of the underlying good) is in sharp contrast to bonds and stock markets where all trades are financial. However, physical and financial commodity markets are, as expected, strongly related.”

“Political upheavals in some countries, economic mutation, new environmental regulation, a huge rise in the consumption of commodities in countries such as China and other structural changes have contributed to increase the volatility of supply and prices. This has made hedging activities (through forwards, Futures and options) indispensable for many sectors of the economy, the airline industry in particular being an important example.”

“Consider a standard situation where the seller is a producer (e.g., of copper) and the buyer a manufacturer: in general, they never meet and, even if they did, would rarely agree on prices, timing and so forth. Hence the existence of intermediaries who play the role of go-between, are prepared to take delivery of goods that may not resell immediately and organize the storage and shipping.”

“A forward contract may be generically described as an agreement struck at date 0 between two parties to exchange at some fixed future date a given quantity of a commodity for an amount of dollars defined at date 0. A Futures contract has the same general features as a forward contract but is transacted through a Futures exchange. The clearing house standing behind that exchange essentially takes away any credit risk from the positions of the two participants engaged in the transaction.”

“Futures contracts serve many purposes. Their first role has been to facilitate the trading of various commodities as financial instruments. But they have from the start been providing a hedging vehicle against price risk: a farmer selling his crops in January through a Futures contract maturing at time T of the harvest (say, September) for a price defined on 1 January has secured at the beginning of the year this amount of revenue. Hence, he may allocate the proceeds to be received to the acquisition of new machinery or storage facilities and, more generally, design his investment plans for the year independently of any news of corn oversupply possibly occurring over the 9-month period.”

defined on 1 January has secured at the beginning of the year this amount of revenue. Hence, he may allocate the proceeds to be received to the acquisition of new machinery or storage facilities and, more generally, design his investment plans for the year independently of any news of corn oversupply possibly occurring over the 9-month period.”

“A forward contract is an agreement signed between two parties A and B at time 0, according to which party A has the obligation of delivering at a fixed future date T an underlying asset and party B the obligation of paying at that date an amount fixed at date 0, denotedand called the forward price for date T for the asset. Note that this price is not a price in the sense of the price of a stock, but rather a reference value in the contractual transaction. If the underlying asset is traded in a liquid market, the no- arbitrage condition between spot and forward markets at maturity implies that:

If the value at date T of the Futures contract maturing at that date was different from

the spot price, an arbitrage opportunity would be realized by buying in one market and selling immediately in the other.

“Forward and Futures prices on the same underlying asset with the same time to expiry are different because of taxes, transaction costs and other important elements, such as the impact of credit risk on the one hand and stochastic interest rates on the other hand. In practice, they remain very close to each other since the fluctuations of the underlying commodity represent the most important explanatory factor. Except when stated otherwise, we will view the two prices as the same in a first-order approximation.”

“Futures markets were originally set up to meet the needs of hedgers, namely farmers who wanted to lock in advance a fixed price for their harvests.”

“While hedgers want to avoid exposure to adverse movements of the price of a commodity which is part of their manufacturing process in the economy, speculators wish to get exposure to commodity price moves (i.e., take risks in order to make profits).”

“Arbitrage opportunities are very desirable but not easy to uncover and they do not last for long. If a given instrument is underpriced, buying activity will cause the price to rise up to a value which is viewed by the market as the ‘‘fair’’ price and at which there will be no more excess demand.”

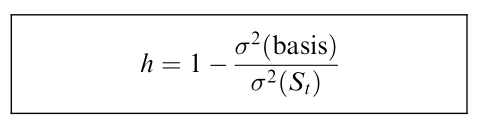

“Understanding basis risk is fundamental to hedging. Basis is defined as:

is usually quoted as a premium or discount: the cash price as a premium or discount

to the Future price. The basis is said to be one dollar ‘‘over’’ Futures if the spot price is one dollar

higher than the Futures price.”

“Since hedgers are trying to eliminate price risk, the classical measure of the effectiveness of hedging a spot position with Futures contracts is defined by:

The closer h is to one, the more effective the hedge.”

“Commodities and commodity markets have undergone dramatic changes over the last few years, with the deregulation of gas and electricity markets, the boom in South American production of soybean and the arrival of new actors in the coffee market. Countries like China are absorbing an increasing percentage of world commodity production and shifting up demand figures. Liquidity has increased in all Futures contracts, in particular for energy commodities which represent today the highest volume of traded Futures. This translates into higher volatility and price risk in all markets; hence, more hedging activities become necessary in all sectors of the economy, from the agrifood business to airline companies.”

—–

Commodity price risk is a central feature of the modern global economy. Every commodity is traded on a spot market, but growing volatility in supply and prices—driven by geopolitics, structural economic shifts, environmental regulation, and surging demand from countries like China—has made risk management unavoidable.To enable large-scale trade, commodity markets had to become standardized. Differences in quality, quantity, and delivery terms made direct producer–buyer transactions impractical. This led historically to organized exchanges and the rise of intermediaries who manage storage, transport, and timing mismatches. Standardization ultimately allowed commodities to be traded not only physically but also financially, a key distinction from equities and bonds, which are purely financial instruments. Despite this difference, physical and financial commodity markets remain tightly linked.

Forward and Futures contracts emerged as the primary tools for managing commodity price risk. A forward contract is a bilateral agreement to exchange a commodity at a fixed future date for a price agreed today. Futures contracts serve the same economic purpose but are traded on exchanges, with clearing houses eliminating counterparty credit risk. While forwards and Futures may differ slightly due to taxes, transaction costs, credit risk, and interest rates, in practice their prices are usually very close.

The original purpose of Futures markets was hedging. Producers and consumers use them to lock in prices and stabilize cash flows, enabling planning and investment independent of future price shocks. Speculators, in contrast, deliberately take on price risk in the hope of profit, providing liquidity to the market. Arbitrageurs enforce consistency between spot and Futures prices by exploiting mispricing, ensuring that deviations do not persist.

A critical concept for hedging is basis risk—the difference between the spot price and the Futures price. Since hedges are rarely perfect, the effectiveness of a hedge depends on how closely Futures price movements offset spot price movements. Hedge effectiveness is commonly measured by how close the hedge ratio is to one.

Overall, commodity markets have become more liquid, more financialized, and more volatile. Energy markets in particular now dominate Futures trading volumes. As volatility and price risk increase across commodities, hedging through derivatives has become indispensable across the economy, from agriculture to manufacturing to airlines.

-

My first review will cover several chapters of Commodities and Commodity Derivatives: Modeling and Pricing for Agriculturals, Metals and Energy by Hélyette Geman.

-

I will read and review one book or long article every sixty days that covers the fundamentals of electricity price forecasting and price forward curve construction.

-

I am interested in the state of the art in spot price forecasting and in the generation of price forward curves (PFCs). One of the main purposes of this blog is to develop and present the essential knowledge related to these topics.